Is the Federal Reserve’s New Shake-Up Good or Bad for Your Retirement Income?

By Tom Dupree, Founder, Dupree Financial Group

Short answer: it’s genuinely both, and which one matters more depends on whether your retirement income is built to keep pace with rising costs. New Federal Reserve Chair Kevin Warsh has launched a formal, five-part review of how the Fed operates — covering everything from how it talks to markets, to how it collects the inflation data that moves interest rates, to whether artificial intelligence is quietly reshaping the economy in ways the old playbook never anticipated.

On this week’s episode of The Financial Hour, James Dupree, Mike Johnson, and Michael Dawahare sat in to break down what this shake-up actually means — and, more importantly, what it means for anyone relying on their portfolio to produce real, spendable income in retirement.

Key Takeaways

- A new Fed chair is auditing the Fed itself — five task forces are reassessing communications, the balance sheet, data quality, and the inflation target.

- The Fed’s own bond portfolio carries an unrealized loss in the hundreds of billions — proof that duration risk applies to everyone, including the Fed.

- AI is cutting both ways on inflation — boosting productivity in some areas, raising input costs like memory chips in others.

- A tariff-driven price bump and true monetary inflation are not the same thing, and the difference matters for how policymakers respond.

- Income that doesn’t grow — money markets, CDs, old bonds — quietly loses ground to rising costs every year it sits still.

Who Is Kevin Warsh, and Why Is He Changing How the Fed Operates?

Kevin Warsh has been a student of the Federal Reserve for most of his career, and one of his first moves as chair was to launch five task forces to reassess the institution’s core functions: communications, balance sheet policy, data quality, productivity and jobs (including AI), and the inflation framework itself. According to CNBC’s reporting on the review, the task forces are directed to start from first principles and question existing practice rather than simply fine-tune it — Brown Brothers Harriman strategist Scott Clemons described the approach as “regime change, but in a velvet glove.”

The philosophy behind it is simple: stop, assess, and pivot where needed — the same discipline any well-run company applies when a board challenges management on why things are done a certain way. Warsh is asking the Fed to do that to itself, publicly, for the first time in a long time.

What Did the Federal Reserve Get Wrong in 2008 and 2021?

To understand why this review matters, it helps to look at the Fed’s actual track record. In 2006 and 2007, as the housing market was cracking, the Fed’s regional offices were on record saying there was no housing problem. There was. Then, in the aftermath of the 2008 financial crisis, the Fed held interest rates near zero for over a decade — a policy commonly called ZIRP — creating what our team described on-air as a “wet blanket” over markets that made honest price discovery difficult.

The more recent example is fresher: in 2021, as trillions in pandemic stimulus moved through the economy, the Fed described the resulting price increases as “transitory.” They weren’t. Prices rose at the fastest pace in decades, and by the time policy caught up, households had already absorbed the damage — a miss the current review is squarely aimed at preventing from happening again.

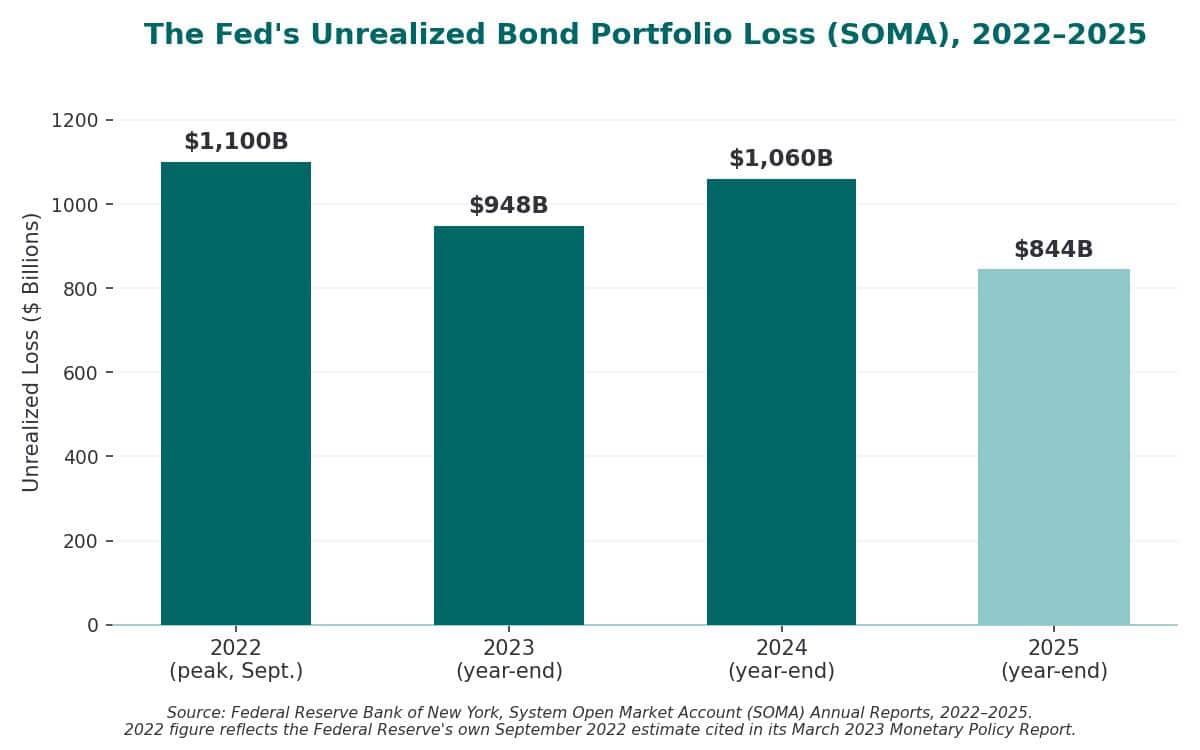

Why Does the Fed Have a Balance Sheet Loss in the Hundreds of Billions?

Source: Federal Reserve Bank of New York, System Open Market Account (SOMA) Annual Reports, 2022–2025.

Here’s a detail that surprises a lot of listeners: the Fed itself is sitting on a large paper loss. During the zero-rate years, the Fed bought enormous quantities of bonds with very low coupon payments as part of a policy known as quantitative easing. When interest rates rose in 2022, the market value of those bonds fell — the same way any bond’s price falls when rates rise. According to the New York Fed’s own 2025 System Open Market Account report, the unrealized loss on the Fed’s securities portfolio stood at $844.2 billion at the end of 2025 — down from over $1 trillion the year before, but still historically enormous.

The Fed can’t easily sell these bonds without disrupting the very bond market it’s trying to stabilize, so for now, it’s simply absorbing the loss. It’s a useful, if uncomfortable, reminder: interest rate risk doesn’t spare anyone — not even the institution that sets interest rates.

The Reframe: What the Fed’s Own Mistake Teaches Retirees About Bonds

Here’s the part of this story that doesn’t show up in the news coverage of Warsh’s review: the Fed’s $844 billion paper loss isn’t just a Washington curiosity. It’s a live demonstration of the exact risk that quietly erodes many retirement portfolios.

The Fed bought long-duration bonds when rates were near zero, on the assumption that those rates — and the value of those bonds — would hold. They didn’t. If the most sophisticated balance sheet in the world can misjudge duration risk that badly, it’s worth asking whether a retirement plan built around the same assumption — that a fixed-rate bond bought today will still meet your needs in ten or fifteen years — is really as safe as it feels. A bond doesn’t know what a gallon of milk costs in 2035. It just pays what it promised to pay in the year you bought it.

This is precisely why our firm’s approach leans on dividend-paying, financially strong companies rather than a bond-heavy “set it and forget it” allocation. A healthy company’s board can raise its dividend as costs rise — a bond’s coupon is frozen the day you buy it. The Fed just proved, at a scale of nearly a trillion dollars, what happens when income doesn’t adjust to a changing rate environment. Retirees don’t have the option of just holding to maturity and calling the loss “unrealized.” That gap has to show up somewhere in a household budget.

Is Artificial Intelligence Good or Bad for the Economy?

One of Warsh’s five task forces is specifically looking at how AI affects productivity and jobs, and our hosts see it as a genuinely mixed picture. On one hand, AI is already making certain kinds of work dramatically more efficient; our hosts pointed to real examples of complex technical projects being completed in a fraction of the time they used to take. Historically, technology has tended to be deflationary — it lowers the cost of producing things over time.

On the other hand, the buildout of AI infrastructure is pushing some costs up right now — memory chips being a clear example, which in turn affects the price of consumer electronics. So the net effect on inflation isn’t a simple yes-or-no answer. It depends on which part of the economy you’re looking at, and over what timeframe.

What’s the Difference Between a One-Time Price Increase and Real Inflation?

This distinction came up repeatedly in the episode, and it matters more than it sounds. A tariff, for example, can raise the price of a specific good once — that’s a one-time adjustment, not ongoing inflation. True inflation, by contrast, is a monetary phenomenon: more money in the system chasing the same amount of goods and services, which pushes prices up broadly and persistently.

Our hosts noted that both the current Fed and Treasury leadership seem comfortable with modest inflation as long as wages are rising faster — a meaningfully different posture than in years past, and one that, if it holds, could support the kind of broader economic growth the country hasn’t consistently seen since before the 2008 financial crisis.

How Can Retirees Protect Their Income From Inflation?

This is where the conversation gets most practical for anyone at or near retirement. Money markets, CDs, and bonds purchased years ago don’t adjust for rising costs — the income they produce today is the same as it was when you bought them, even as your expenses climb. That’s not a flaw in those tools; it’s simply not what they’re designed to do.

An income approach built around dividend-paying, financially strong companies works differently. When the underlying businesses are healthy, they have the ability to grow their dividend payments over time — even during flat or difficult markets — because a board’s decision to raise a dividend is separate from where the stock market happens to be on any given day. That’s the mechanism our team described as the foundation of an inflation-aware retirement income strategy: income with the potential to rise, rather than income that’s frozen in place.

Frequently Asked Questions

Is a little inflation actually a good thing?

Fed and Treasury leadership have signaled comfort with modest inflation as long as wages are rising at a faster rate. The concern isn’t inflation existing at all — it’s inflation outpacing the income people rely on to cover their expenses.

Why did the Fed call 2021 inflation “transitory” when it clearly wasn’t?

The Fed’s framework at the time treated the post-pandemic price spike as temporary, tied to supply chain disruptions expected to resolve quickly. Instead, inflation persisted and accelerated well into 2022, now viewed as one of the Fed’s most consequential misreadings.

Does AI cause inflation or reduce it?

Both, depending on where you look. AI-driven productivity gains tend to be deflationary over time, the way most technology has been historically. But the current buildout of AI infrastructure is pushing up costs in specific areas, like memory chips, in the near term.

Why don’t bonds and CDs keep up with inflation?

A bond or CD generally pays a fixed rate of interest set at the time of purchase. As the cost of living rises afterward, that fixed payment buys less — there’s no built-in mechanism for the income to grow along with your expenses, the same dynamic that produced the Fed’s own unrealized loss.

What should I actually do if I’m worried my retirement income isn’t keeping pace?

Start by getting a clear picture of what you currently own and what income it’s actually producing versus what your expenses look like today. A complimentary portfolio review is designed to give you exactly that picture, with no obligation attached.

The Bottom Line

The Fed rethinking its own playbook is genuinely good news — a clear-eyed institution is better than a defensive one. But the more useful question isn’t what Washington does next. It’s whether your own income is built to grow, or built to sit still while everything around it gets more expensive. That’s a question worth answering before the next rate cycle makes it more urgent, not after.

Ready to See Whether Your Portfolio Can Keep Up?

If you’re not sure whether your portfolio’s income is actually keeping up with what things cost these days, that’s exactly the kind of question a complimentary portfolio review is built to answer. No charge, no pressure — just an honest look at what you own and whether it’s working for you.

Call 859-233-0400 or schedule your complimentary portfolio review. You can also listen to more episodes of The Financial Hour, and learn more about our fee-only, fiduciary approach on our About Us page.

About Tom Dupree: Tom Dupree is the founder of Dupree Financial Group and a 47-year veteran of the investment business. He hosts The Financial Hour, covering the financial topics that matter most to retirees and those approaching retirement in plain English, without the Wall Street spin.

Regulatory Disclaimer

Dupree Financial Group is a Registered Investment Adviser (RIA) registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. The information presented here is for educational purposes only and does not constitute investment advice, a solicitation, or an offer to buy or sell any security. Past performance is not indicative of future results. Investing involves risk, including the possible loss of principal. Listeners and readers should consult with a qualified financial professional before making any investment decisions.