That is the trap. And it is compounded right now by something called recency bias — the tendency to assume that what has been happening will keep happening. Markets have gone up for a long time. New IPOs are capturing attention. There is enthusiasm in the air. And enthusiasm breeds complacency. People assume the funds that have been performing well will keep performing well, without checking whether the companies inside them still deserve their valuations.

Should You Sell When the Market Drops? The Case for Staying Invested During Volatility

By Tom Dupree, Founder — Dupree Financial Group | Last Updated: June 2026 | dupreefinancial.com

I have been managing money for 47 years. In that time, I have watched investors survive crashes, recessions, a pandemic, and a handful of moments that felt — from inside them — like the whole thing was coming apart.

The ones who came through it best almost never did it by being clever about timing. They did it by staying invested when everything in them said to get out.

That sounds simple. It is not. Because when the market is dropping and the financial news is relentless and your account balance is going the wrong direction, selling feels like the rational move. It feels like you are finally doing something instead of just watching it happen to you.

But here is what I have seen happen to the investors who acted on that feeling. They sold. They waited for things to settle down. And by the time they felt safe enough to get back in, the market had already recovered most of the ground they were trying to protect themselves from losing. The exit was imperfect. The re-entry was worse. And the cost of both — measured in missed growth and missed dividends — followed them for years.

This post is about staying invested during market volatility — what that actually means in practice, when it is right to hold, and how dividend income changes the calculation entirely for anyone approaching or already in retirement.

Key Takeaways

- The best market days happen during the worst ones. Research shows 76% of the market’s best single days occur during bear markets or in the first two months of a new bull run. Exiting to avoid the declines means missing the recoveries.

- Dividends solve a problem index funds cannot. Income from your holdings lets you cover living expenses in retirement without selling assets at depressed prices — the key to managing sequence of returns risk.

- Valuation is not the same as market fear. The right reason to sell a position is a change in the company’s underlying value or business fundamentals — not a falling stock price.

- Cash is a valuation call, not a retreat. Holding more cash than usual signals that current prices don’t offer enough compelling opportunities — it preserves capital and creates optionality.

- Knowing what you own is not optional. Without understanding your underlying holdings, market price movements become your only signal — and that is exactly when emotional decision-making takes over.

Why Panic Selling Costs More Than the Drop Itself

There is a number I come back to every time markets get rough, and it never stops being striking.

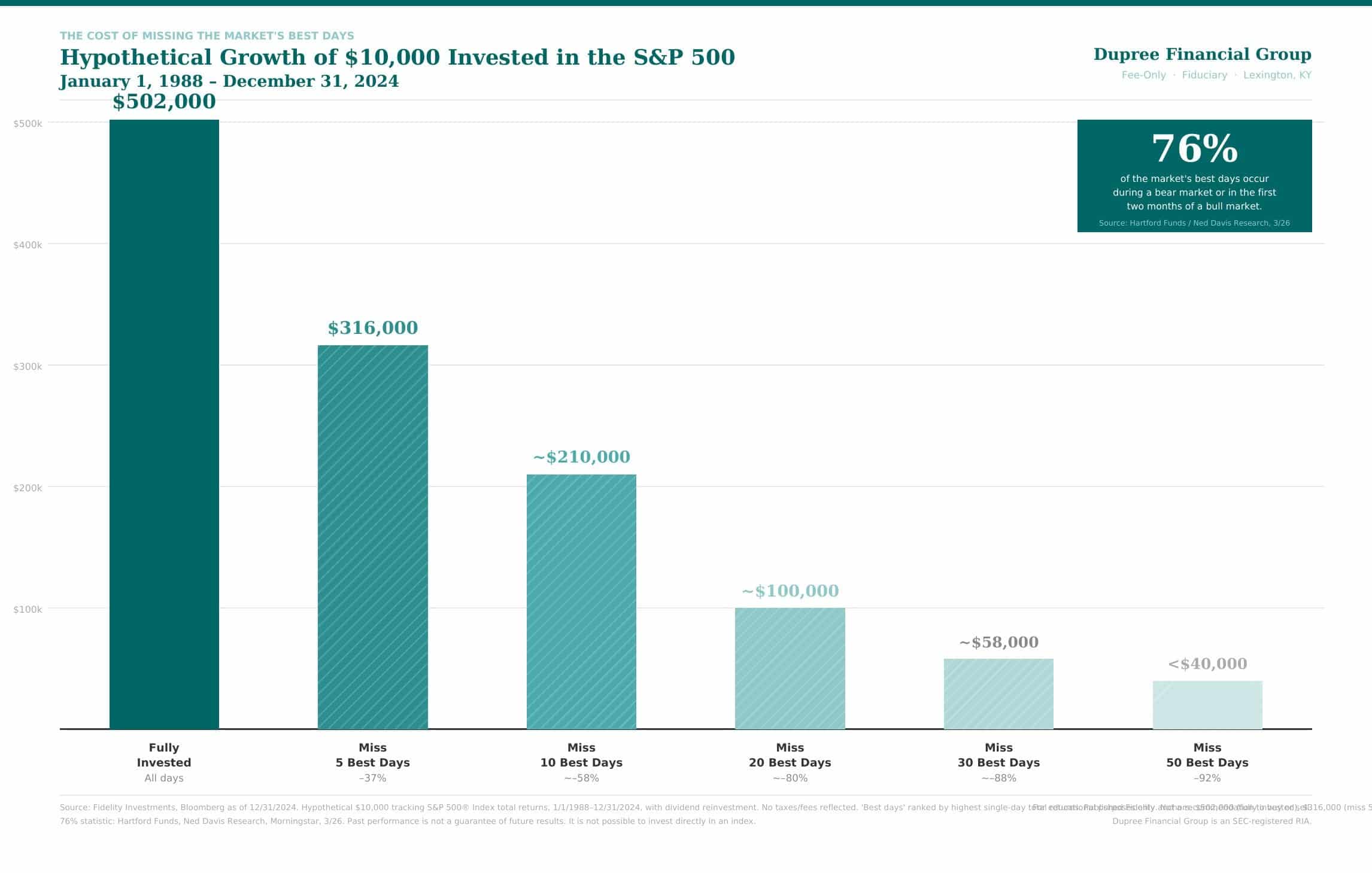

Seventy-six percent of the stock market’s best single days over the past 30 years occurred either during a bear market or in the first two months of a new bull market. Think about what that means in practical terms. The days that do the most to rebuild a damaged portfolio almost never arrive when things feel safe. They arrive in the middle of the chaos — often within days of the worst declines.

Fidelity’s data makes the cost of missing those days concrete. A hypothetical $10,000 invested in the S&P 500 from 1988 through 2024 grew to over $500,000 for a buy-and-hold investor. Miss just the 5 best days over that entire period and that gain shrinks by 38%. Miss the 50 best days and the $500,000 portfolio is worth under $40,000. Same time period, same starting amount — the only difference is whether you were in the market on a handful of days you could not have predicted in advance.

Most investors who exit during a decline are not planning to miss 30 or 40 good days. They are planning to get back in when things settle down. But the settling down and the best days are not separate events. They are the same event. The investor who moved to cash in March 2020 — when the news was genuinely terrifying — locked in losses right before one of the fastest recoveries in market history. The recovery did not wait for the all-clear signal.

“Income from the portfolio tilts the table in your favor — it puts time back on your side while you wait for price appreciation.” — Tom Dupree, Dupree Financial Group

I have watched this play out with investors who were half right. They called a decline correctly. The market went down, just as they predicted. But it did not go down as far as they expected, so they never pulled the trigger to buy back in — and then the market moved up, and their window closed. Being right about direction and wrong about magnitude still cost them. A partial win that turns into a full loss.

The ego piece matters too. Once someone has made a public call to get out, getting back in means admitting the exit was a mistake. I have seen investors stay on the sidelines for years rather than admit they were wrong. The market moved on. They did not.

Why Retirement Investors Face a Different Problem Than Everyone Else

For investors who are still accumulating — still adding to their portfolios every month — a market decline is a nuisance. It may even be an opportunity. They are buyers, and lower prices mean they get more for their money.

For investors who are drawing from their portfolios to pay for their lives, a market decline at the wrong time is something far more serious. There is a specific name for it: sequence of returns risk.

Retirement researcher Wade Pfau has quantified the magnitude of this effect: approximately 77% of a portfolio’s final retirement outcome can be explained by the returns of just the first ten years. The first decade is not just an early chapter in a long story. For most retirees, it is most of the story.

Fidelity puts a dollar figure on it. Two hypothetical retirees each start with $1 million and withdraw $50,000 a year, experiencing the exact same set of annual returns over 30 years — just in reverse order. The retiree whose strong years come first finishes with over $3 million. The one whose losses arrive first sees the portfolio gone by year 27. Same returns. Same withdrawals. Different sequence. Completely different life.

This is the problem that average returns and long-term market graphs do not show you. They assume you are a lump sum sitting patiently in the market for decades, untouched. Most retirees are not that. They are drawing money out regularly. And when you are drawing money out, the order of returns matters as much as the average of them.

I have said this on the show, and I will say it again here: Wall Street will show you long-term averages because averages look good. But averages do not pay your electric bill in a down market. What pays your electric bill is income — dividends arriving in your account regardless of what prices are doing.

How Dividend Income Changes the Calculus on Staying Invested

When a stock pays a meaningful dividend, the decision to sell it is not just a price decision. It is also a decision to give up a stream of income — potentially forever. That changes the analysis.

Take a position like AGNC, a mortgage REIT that carries an above-average dividend yield. The price moves around. But the income it generates is meaningful, consistent, and independent of what the stock is doing on any given Tuesday. Selling to avoid price volatility means giving up that income. And over time, the income you give up typically exceeds whatever you thought you were protecting yourself from.

The same logic applies to long-held pipeline stocks. The dividend yield on those positions for new buyers today is far less attractive than it was when we established our stake years ago. But we have continued to hold because the income stream we are receiving — based on our original cost basis — is still excellent, and we do not believe we can replicate that income at current prices.

This is the part of portfolio management that does not show up in most financial planning software. It is not just about what a stock is worth today. It is about what it pays you while you hold it. A stock that generates consistent income buys you time — time to wait through price volatility without being forced into a sale, time for the thesis on the business to play out, time for the market to re-price something it has temporarily misjudged.

That is what I mean when I say income puts time back on your side. In retirement, time is the asset you have the least of. Dividends give some of it back.

When Does It Actually Make Sense to Sell?

Staying invested does not mean holding everything forever. The argument against panic selling is not an argument against selling. It is an argument for selling with a reason — a real, company-specific, valuation-grounded reason.

We trim positions when the math stops making sense. Earlier this year, we reduced our oil company holdings. Not because oil was going to collapse. Not because the market scared us. But because when we looked at the valuations, the stocks had gotten expensive relative to what the underlying business was actually producing. The commodity prices and the stock prices had diverged to a point where the math no longer worked in our favor. That is a logical reason to take some off the table.

We also sold Kroger. That one took a little more explanation to clients. Kroger looks like a grocery company. And it is. But a meaningful portion of Kroger’s profitability runs through its fuel stations. When gasoline prices rise and consumption falls, that profit driver weakens. Meanwhile, the grocery side of the business had to contend with sharply higher food prices — which does not help unit volume. The business model was under real pressure on two fronts. The stock price had not fully caught up with that reality. So we sold.

Notice what both of those decisions have in common. Neither one was driven by where the S&P 500 was trading or what the Federal Reserve said last week. Both were grounded in a specific company, a specific business dynamic, and a specific valuation judgment.

That process has to be built into how you manage a portfolio from the beginning — not invented in the middle of a panic. Investor Howard Marks captured it well: “You can’t predict, but you can prepare.” The preparation is knowing, in advance, what would cause you to sell a given holding. Price hitting a specific valuation threshold? A change in the company’s earnings power? A dividend cut? Define it before the market gets rough, so you are not making those decisions under pressure.

“You can’t predict, but you can prepare.” — Howard Marks, investor and co-founder of Oaktree Capital Management

What a Large Cash Position Really Signals

Right now, Dupree Financial Group holds roughly 35% of client portfolios in cash and short-duration bonds. That is well above our historical norm. And I want to be specific about what that means and what it does not mean.

It does not mean we think the market is about to crash. Nobody knows that. It does not mean we are sitting on our hands. Cash in this rate environment still generates a return.

What it does mean is that when we look at current equity valuations broadly — across the sectors we know well, the companies we follow closely — we are having a harder time finding things we want to own at current prices. Valuations look stretched relative to what the underlying businesses can reasonably deliver. And when we cannot find things worth buying at the price the market is asking, holding cash is not a failure of nerve. It is a rational response to what the market is offering.

Here is the result we can point to: portfolios with that 35% defensive allocation have delivered returns comparable to some fully-invested indexes. Protecting retirement capital while generating competitive returns with meaningfully less risk — that is not a bad outcome. It is actually the whole point.

We are not a hedge fund required to be 100% deployed. We are managing retirement money. That means the risk profile — not the potential return — has to come first. The sell discipline flows from the risk profile. Everything else follows from that.

The Real Problem With Most 401(k) Portfolios

I talk to a lot of people approaching retirement who, when I ask what they own, tell me the names of their funds. Fidelity Target Date 2025. Vanguard Total Market. Some growth fund their HR department selected in 2011.

They do not know the underlying holdings. They do not know their actual sector exposure. They do not know what percentage of the fund is in companies that have become very expensive over the past few years, and what percentage is in companies that are still reasonably priced. They do not know whether any of their holdings pay meaningful dividends.

What they do know is the price of the fund. And when the price goes down, that is the only signal they have. No context, no analysis, no understanding of whether the drop reflects something real or just a broad market reaction that will pass. So they feel fear. And some of them act on it.

That is the trap. And it is compounded right now by something called recency bias — the tendency to assume that what has been happening will keep happening. Markets have gone up for a long time. New IPOs are capturing attention. There is enthusiasm in the air. And enthusiasm breeds complacency. People assume the funds that have been performing well will keep performing well, without checking whether the companies inside them still deserve their valuations.

The major indexes have also undergone significant rotation lately — the companies that led for the past several years are no longer the leaders. If you hold a broad index fund and have not looked inside it recently, the portfolio you thought you owned may be meaningfully different from the one you actually own today.

Know what you own. Why you own it. And what conditions would cause you to make a change. That is not a complicated framework. But without it, you are flying on instruments you cannot read in weather you did not see coming.

What to Actually Do: A Framework for Staying Invested Wisely

Here is how we think about it at Dupree Financial Group — and how I would encourage any retirement investor to think about it:

- Understand each holding before volatility arrives. Know what every position is, what it pays, what would make you sell it, and what would make you add to it. This should be settled before the market gets rough, not improvised in the middle of it.

- Build income into the portfolio. Dividend-paying holdings provide cash flow that lets you meet retirement expenses without selling assets at depressed prices. This is the most direct and reliable way to manage sequence of returns risk.

- Sell on valuation, not on fear. If the stock price has risen well beyond what the business justifies — or if something has fundamentally changed in how the company earns money — that is a reason to trim or exit. A declining stock price, by itself, is not. In fact, a declining price in a good business is often a reason to consider adding.

- Treat cash as a judgment about opportunity, not a retreat from markets. Holding cash is a statement that you do not currently see enough value to deploy it. It keeps you liquid for when better opportunities appear. It is not the same as giving up on investing.

- If you do not understand your portfolio, get help before the next downturn. You should be able to articulate, in plain terms, what you own and why. If you cannot, find someone who can help you get there. Not a product salesperson — a fiduciary who charges a fee to give you advice that is actually in your interest.

Frequently Asked Questions

Should I sell my investments when the stock market drops?

Selling during a market drop is one of the costliest decisions a retirement investor can make. Research from Hartford Funds shows that 76% of the stock market’s best single days occurred during a bear market or in the first two months of a new bull market. Investors who exit to avoid the declines frequently miss the recoveries that follow almost immediately — often within days. Unless there is a fundamental, company-specific reason to sell, staying invested has historically been the better outcome.

How does dividend income protect a retirement portfolio during volatility?

Dividend income provides a return that doesn’t depend on stock prices rising. When markets fall, dividends continue to arrive and can cover living expenses without forcing a sale at depressed prices. For retirement investors managing sequence of returns risk, income from dividends reduces or eliminates the need to liquidate holdings at exactly the wrong moment — which is when the long-term damage typically gets done.

What is the right way to decide when to sell a stock?

The sell decision should be grounded in company-specific valuation and fundamentals — not broad market fear. A position may warrant trimming when its price has risen well beyond what the underlying business justifies, when the dividend yield for new buyers has become unattractive, or when the company’s core business model has changed materially. Selling because the market is falling, absent a specific reason tied to that company, is rarely the right call.

Can you successfully time the stock market to avoid losses?

Consistent broad market timing has an extremely poor track record. Fidelity’s analysis shows that a hypothetical $10,000 invested in the S&P 500 from 1988 through 2024 grew to over $500,000 for a buy-and-hold investor — but missing just 5 of the best days reduced those gains by 38%, and missing the 50 best days left the investor with under $40,000. The best and worst days cluster together, so exiting to avoid the bad ones typically means missing the good ones too. Valuation analysis on individual holdings is a more reliable guide than macro market calls.

What is sequence of returns risk and why does it matter in retirement?

Sequence of returns risk is the danger that poor market returns early in retirement — combined with ongoing withdrawals — permanently damage a portfolio before it can recover. Retirement researcher Wade Pfau found that roughly 77% of a portfolio’s final outcome is explained by just the first ten years of returns. Fidelity’s research puts a dollar figure on it: two hypothetical retirees, each starting with $1 million and withdrawing $50,000 a year, experience the same returns over 30 years but in reverse order — one finishes with over $3 million, the other runs out of money by year 27. A dividend-income approach helps manage this risk by providing cash flow that reduces forced selling during down markets.

The Close: What the Market Does Not Owe You

I learned this one the hard way early in my career, and it cost me personally and it cost some of my clients. The market does not care that you own something. It does not reward loyalty. It does not notice that you’ve held a position through three bad quarters and deserve a good one.

The market is just the market. In the long run, it prices things with reasonable efficiency. In the short run, it is highly inefficient — driven by fear, greed, momentum, and a hundred other forces that have nothing to do with the underlying value of the businesses you own.

Your job — and our job — is to understand value well enough to hold when the market underprices something good, and to step back when it overprices something we used to like. To get paid while we wait, through dividends. To stay optimistic enough to keep doing this at all, because investing requires belief that businesses will create value over time and that human ingenuity will keep generating things worth owning.

None of that is possible if you sell every time it gets uncomfortable.

Staying invested is not a passive act. Done right, it is one of the most disciplined things an investor can do.

Related Reading and podcasts:

Schedule a Complimentary Portfolio Review

If you’re not sure whether your portfolio is built to generate income through market volatility — we’ll take a look. No charge. No pressure. Just an honest conversation about what you own and whether it’s working for you.

Call: 859-233-0400 | Visit: dupreefinancial.com

About the Author

Tom Dupree is the founder of Dupree Financial Group and has worked in the investment industry for 47 years. Dupree Financial Group is a fee-only, fiduciary Registered Investment Advisory firm based in Lexington, Kentucky, specializing in income-generating, dividend-paying portfolios for retirees and those approaching retirement. Tom hosts The Tom Dupree Show, a weekly radio program and podcast covering retirement investing topics in plain English.

Dupree Financial Group is an SEC-registered investment adviser. Registration does not imply a certain level of skill or training. The information presented is for educational purposes only and does not constitute investment advice. All investing involves risk, including the possible loss of principal. Past performance is not indicative of future results. Securities mentioned are for illustrative purposes only and are not a recommendation to buy or sell any security. Please consult a qualified financial professional before making any investment decisions.