Congratulations, you have built up some substantial assets in your 401(k) plan with your employer, and now that you are contemplating retirement you have several choices…

First, you could just liquidate it completely and take it all in the form of cash.

Let’s just assume that since you are reading this you don’t want to take that option!

If they allow it, you could keep it with your employer and leave it in that 401(k).

You may be fairly comfortable with the current plan and might be leaning that way.

But there is a third option that might just make the most sense. You could roll those assets into an IRA.

Let’s take a look at five reasons that this third option might just be best for you. Rolling those retirement assets to an IRA can give you a lot of flexibility and benefits. Some of which you just can’t get from your 401(k).

A Financial Advisor May Provide Much Better Communications Than Your 401(k) Plan

Possibly the biggest reason to roll your 401(k) plan to an IRA is the consistency in communications that you get from a firm like Dupree Financial Group, LLC. It is your money, and it is important to have that you have an active partner in managing your assets.

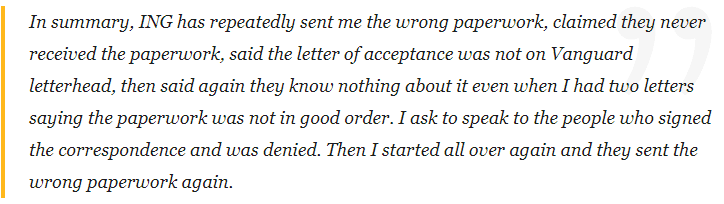

Just take a look at the following testament from a 401(k)-plan participant, let’s call him Ralph, when he was just trying to perform a small rollover:

Even the simplest of tasks can become a nightmare when you don’t have a financial advisor that works for you, and not for a “plan”. Ralph did finally get his 401K sorted out, but the process took months and hours of legwork.

You Will Have More Investment Options With an IRA

Have you ever just wanted to own a specific stock? Or maybe avoid a another one? Well, you can!

With a 401(k) plan, you only have the option to invest in the offerings of that specific plan. This often equates to no more than a couple dozen mutual funds. And these funds may not fit your investment plan at all.

If you roll those assets over to an IRA and receive advice from a financial advisor, you open up a full suite of investment options. Instead of being caged in with a few choices of funds, you will have the opportunity to invest in specific companies. You will invest in companies that meet your personal long-term goals.

Maybe you seek value-oriented investments that generate the cash flow that you need in retirement like we invest in at Dupree Financial Group.

Maybe you want to purchase individual corporate bonds. Now that yields are up you might even want some exposure to several investment vehicles.

If you leave that money sitting in your 401(k) plan, you very likely won’t have those options and you will be forced to stay with only the offerings of that particular plan. And sometimes you don’t even know what the offerings actually are.

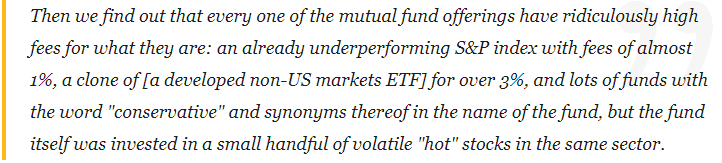

Here is a testimonial from a 401(k)-plan member, “Ludd”:

According to “Ludd”, her 401(k) plan featured a fund labeled conservative and it did not meet what she might call conservative. With a direct investment in an IRA, she would be able to know what stocks she actually owned.

Avoid Federal Tax Withholdings Mandates

When you take a distribution for your 401k plan, you are forced… that’s right… forced to withhold 20% of your distributions and pay the IRS immediately. It doesn’t matter what your effective tax rate is, the IRS will get some of that money right now.

By rolling your 401k plan to a traditional IRA with a trusted financial advisor, you can defer taxes on distributions. That doesn’t mean you have to defer taxes. You can withhold as little or as much as you would like. However, it is a fantastic option to have. And it is an option do not have if you keep the assets in a 401k.

Your 401(k) Plan Beneficiary Designations are Governed By ERISA

There is a huge difference between your 401k plan and an IRA with respect to beneficiaries. There is a federal law, the Employee Retirement Income Security Act (ERISA), that governs 401k and other retirement plans. Under ERISA, your spouse is entitled to half of these retirement assets in the event of your death.

That’s right… half!

It doesn’t matter what your beneficiary designation is on your 401(k) plan. Unless they have signed and “properly executed” a spousal waiver, they will get at least half of those assets upon your death.

For some couples that might be the preferred distribution. However, if you have children from a previous marriage and have since remarried, this can make your situation different from what ERISA intended.

If you have been divorced, you may very well have changed your beneficiary designation to your children or other family members. You might not realize that, when you remarry, your new spouse will supersede that designation. They could very well receive half of your retirement assets upon your death.

However, if you roll those assets to an IRA with a financial advisor, you can avoid this issue. Federal courts have confirmed time and time again that spouses do not have ERISA rights with respect to inherited IRA assets. Rather, it is State law that determines those rights. In most cases, you can define precisely who will inherit these funds by beneficiary designation.

If having the flexibility to alter your beneficiaries is important to you, you should contact us to help ensure that you have clearly defined your intentions.

Rolling Your 401(k) Plan to an IRA Simplifies Your Required Minimum Distributions

You might not be 72 yet but when that day comes, you will be required by law to take the minimum distributions from your tax-sheltered accounts.

The IRS wants its tax revenue, so you must take distributions each year whether you need it or not. They even have a ‘simple’ table to help you calculate exactly how much you are required to take.

There is a great chance that in addition to your 401(k) plan, you have multiple other retirement accounts. You may even find yourself with multiple 401(k) plans from multiple employers. If you haven’t rolled those assets over when you changed careers in the past, you might face this issue.

You may not realize this, but you will be required to take a distribution from each of those accounts separately each year. If you do not roll those assets to an IRA, each and every year you will be required to take a distribution from each one of those accounts individually.

And if you don’t, you will get a big penalty.

The penalty for not doing so can be as much as 50% of what the IRS has designated as your required minimum distribution (RMD).

You can simplify your life by rolling these accounts to an IRA.

It doesn’t matter if you have 1, 5, or 25 different traditional IRA accounts. You have flexibility in choosing which of your several accounts to actually receive your distribution. Sure, you can take them for each account, but you are not required to do so. The only thing that matters is that you take, in aggregate, the minimum as required by law.

This flexibility can come in very handy.

Let’s say that you have a particular investment that doesn’t fit well with your current strategy or situation and said the investment is held in only one of your accounts. With IRA’s you can sell that one investment and receive your distribution from that account without having to modify or partially liquidate anything else… talk about flexibility!

Roll Your 401(k) Plan to an IRA with Dupree Financial Group

If you think you might want the flexibility that an IRA can provide as you approach retirement, you should contact Dupree Financial Group for a free consultation. We have been in the business of providing investment consultation and 401(k) rollovers for almost two decades.

As financial advisors, we perform due diligence on every company that we buy for our clients. We have a working knowledge of the companies in which we invest our client’s hard-earned money.

With Dupree Financial Group on your side, you will have consistent communications with respect to your investments. We will help you with the regulatory requirements. And we will help you formulate a long-term strategy for managing your assets into retirement and beyond. It never hurts to get a second set of eyes on your portfolio.